Credit utilization is widely considered the second most impactful factor in your FICO score, accounting for roughly 30% of the total calculation. Despite its importance, it is often the most confusing metric to manage effectively. Most people only check their utilization after their score has already dropped, or they rely on a static credit utilization calculator found on a random website, which requires manually re-entering balances and limits every single month.

To truly optimize your credit score, you need to move from reactive checking to proactive management. Instead of treating this calculation as a one-off math problem, you can build a dynamic system in Quadratic. By creating a living dashboard that syncs with your real balances, you can monitor your usage in real-time, simulate payments before money leaves your account, and catch utilization spikes before they are reported to the bureaus.

How to calculate credit utilization (the math behind the score)

Before building a system to automate the process, it is helpful to understand the underlying logic. Search engines and financial blogs often overcomplicate the definition, but the math is straightforward.

The credit utilization ratio is the percentage of your total available credit that you are currently using. The basic formula is: (Total Debt / Total Credit Limit) * 100.

For example, if you have a credit card with a $10,000 limit and a balance of $2,500, your utilization is 25%. Financial experts generally recommend the "30% rule," suggesting that you keep your utilization below 30% to maintain a healthy score, though high achievers often aim for less than 10%.

While the math is simple, the execution is difficult. Most people have multiple cards with different limits, different balances, and different statement dates. A standard 30 percent credit utilization calculator on the web can tell you where you stand today, but it cannot track how those numbers fluctuate throughout the month or help you plan strategic payments across a complex portfolio.

Aggregate vs. per-card utilization

One of the most common misconceptions is that only your total debt matters. In reality, credit scoring models look at two distinct types of utilization, and your calculator needs to account for both.

- Aggregate utilization: This is the sum of all your credit card balances divided by the sum of all your credit limits. This gives you a big-picture view of your debt load.

- Per-card utilization: This measures the usage on each individual line of credit. Even if your aggregate utilization is a healthy 10%, having a single card maxed out at 90% can significantly drag down your score.

A robust credit utilization calculation must track these metrics simultaneously. This is where simple web widgets fail; they rarely allow you to input distinct limits for five different cards to see which specific account is hurting your score. In Quadratic, you can structure your data to flag both aggregate health and individual card risks in the same view.

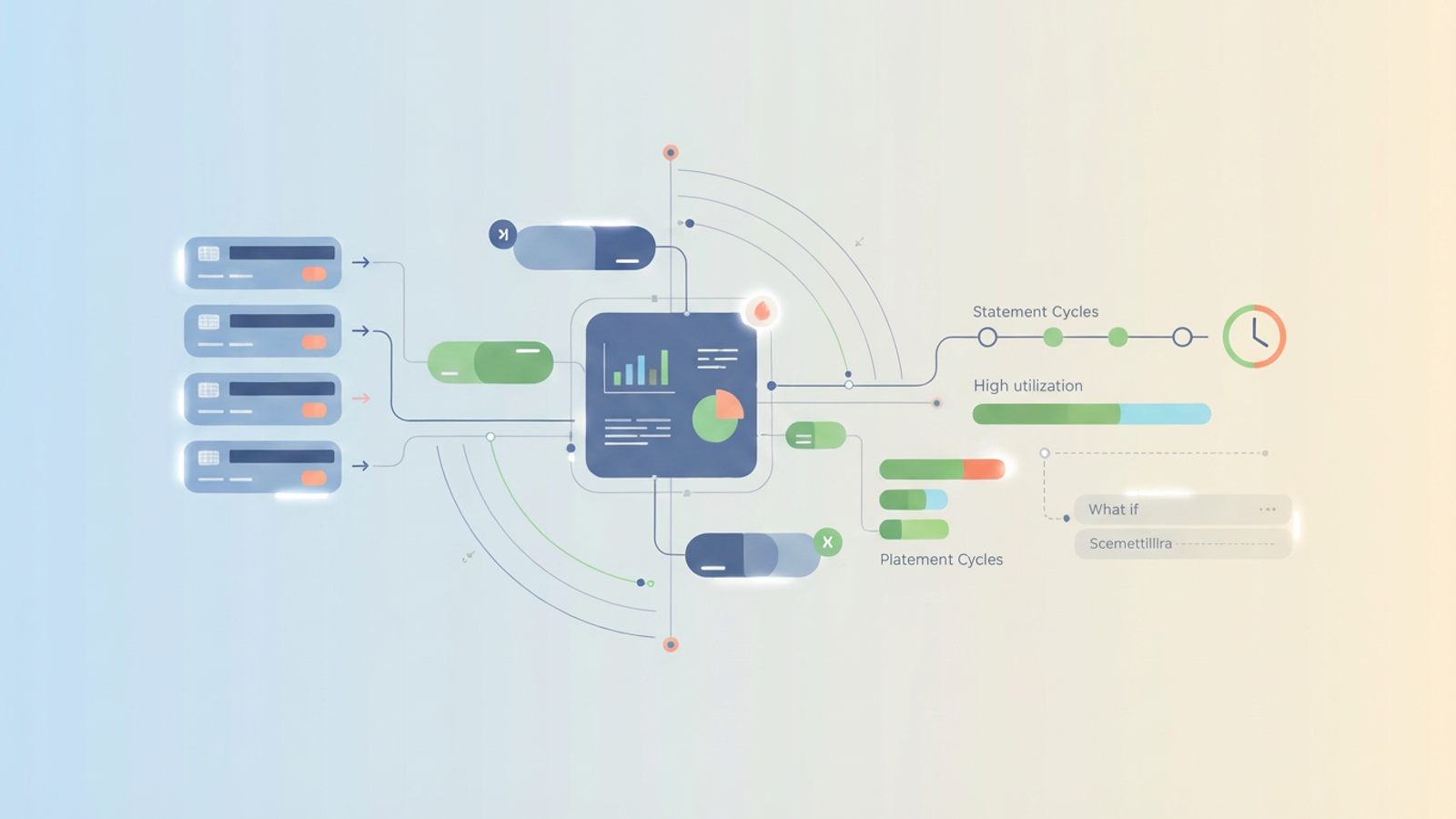

Building your credit command center in Quadratic

The goal is to transition from a passive observer to an active manager of your financial data. By building a calculator in Quadratic, you create a workspace that persists over time, allowing you to update numbers without rebuilding the logic.

Step 1: Syncing balances

The friction of manual data entry is the main reason people stop tracking their credit. In a traditional spreadsheet, you have to log into every bank account, memorize the balance, and type it into a cell, a tedious process that a bank account tracker can simplify.

Quadratic allows you to bypass this friction. Because it integrates with Python and SQL directly in the grid, you can connect to external data sources. Advanced users can use Python scripts to pull transaction data or balances from financial APIs or export CSVs from their banks and drag-and-drop them into the sheet. This ensures that the inputs for your credit utilization ratio calculator are always accurate and up to date without manual transcription errors.

Step 2: Inputting limits

Unlike balances, your credit limits rarely change. You can set up a static column in your Quadratic sheet for the credit limit of each card. This serves as the denominator for your calculations. If you request a credit limit increase, you simply update this single cell, and your entire model recalculates instantly.

Step 3: Automated math and visualization

With your balances (numerator) and limits (denominator) in place, you can set up formulas to calculate credit card utilization automatically. You can create a summary row that sums all balances and limits to show your aggregate percentage, while maintaining individual row formulas for per-card performance.

To make the data instantly actionable, you can apply conditional formatting. For example, you can set a rule that turns a cell yellow if utilization crosses 10% and red if it crosses 29%. This creates a visual "danger zone" indicator, allowing you to see exactly which card needs attention the moment you open your dashboard.

Timing your payments: statement date vs. due date

Math is only half the battle; the other half is timing. A major gap in most generic advice on how to calculate credit card utilization is the failure to distinguish between the "Due Date" and the "Statement Closing Date."

Credit card issuers typically report your balance to bureaus on the statement closing date, not the due date. If you pay your bill in full on the due date, but your statement closed three days prior with a high balance, the bureaus will still see—and penalize you for—that high utilization.

In your Quadratic command center, you can add a column for "Statement Date." By sorting your data based on which statement closes next, you can prioritize payments strategically. If you see a card is at 45% utilization and the statement closes in two days, you know you need to make a payment immediately to lower the reported balance, rather than waiting for the actual due date.

Scenario planning: "what if" analysis

One of the distinct advantages of using a computational canvas like Quadratic is the ability to sandbox your financial decisions. Before transferring money from your savings to pay down debt, you can run a "What If" analysis.

You might ask, "If I put $1,000 toward my Visa and $500 toward my Amex, how does that change my aggregate score compared to putting it all on the Visa?"

By creating a "Proposed Payment" column and linking it to your utilization formulas, you can simulate different payment strategies, such as those used in a debt snowball tracker. This allows you to identify the most efficient way to deploy your cash to maximize your credit score improvement before you actually spend the money, similar to planning with a cash flow calendar.

Tracking utilization trends over time

Static calculators have no memory. Once you close the browser tab, your data is gone. However, financial health is a trend, not a snapshot.

Because Quadratic handles data flexibly, you can store historical records of your utilization month over month. You can use Python to visualize this history, plotting your aggregate utilization on a line chart to ensure you are trending downward, a core component of effective Financial Data Visualization. This shifts your mindset from "putting out fires" to long-term financial optimization, giving you a clear visual record of your progress toward a better credit profile.

Conclusion

Credit utilization is a game of math and timing. While the formula is simple, managing it across multiple accounts with different reporting dates requires a system more robust than a napkin or a web form.

You do not need to do the math manually every month. By building a persistent credit utilization calculator in Quadratic, you turn a static formula into a dynamic system that watches your back. It allows you to centralize your data, visualize your risks, and time your payments for maximum impact.

Start building your own utilization tracker in Quadratic today and take control of your financial data.

Use Quadratic to calculate your credit utilization

- Automate data entry by syncing balances from bank APIs or CSVs, eliminating manual input for each account.

- Track all credit metrics in one place, monitoring both aggregate and individual card utilization simultaneously.

- Visualize risks instantly with conditional formatting that highlights "danger zones" on specific cards or overall.

- Optimize payment strategies by running "what if" scenarios to see the impact of different payment allocations before you spend money.

- Time payments strategically by identifying statement closing dates to ensure lower balances are reported to credit bureaus.

- Monitor progress over time with historical data and visualizations that show your credit utilization trends.

Take control of your credit score. Start building your dynamic credit utilization tracker in Quadratic today. Try Quadratic