Table of contents

- How the avalanche method works (the math vs. the psychology)

- The limitations of standard web calculators

- Building a dynamic debt avalanche calculator in Quadratic

- Modeling "lumpy" payments and hybrid strategies

- Key inputs for your calculation

- Conclusion: From calculation to execution

- Use Quadratic to build a dynamic debt avalanche calculator

Debt repayment is rarely just about paying bills; for the financially conscious, it is an exercise in mathematical efficiency of debt repayment. The goal is not simply to reach zero but to get there while retaining as much of your own money as possible. This is where a debt avalanche calculator becomes an essential tool. By strategically targeting debts with the highest interest rates first, this method minimizes the total interest paid over the life of your loans, effectively shortening your path to financial freedom.

However, the problem with most debt repayment strategies isn't the math—it is the tracking. Standard web-based calculators provide a static snapshot based on a single moment in time. They assume your income, spending, and interest rates will remain constant for years, which rarely reflects the reality of variable income and expenses. To truly optimize your payoff strategy, you need a solution that adapts to your financial life. By building a calculator in Quadratic, you can move beyond static web forms and create a living dashboard that connects to your actual bank data, employs Python for complex logic, and adjusts dynamically as your finances evolve.

How the avalanche method works (the math vs. the psychology)

The debate over the best way to pay off debt usually centers on two primary strategies: the snowball method and the avalanche method. To understand why a data-driven individual would choose the latter, it is important to look at the mechanics of the debt snowball vs avalanche calculator logic.

The snowball method focuses on psychological principles of debt repayment. It suggests listing debts from the smallest balance to the largest, paying off the small ones first to generate quick "wins" and build momentum. While this provides behavioral reinforcement, it ignores the cost of borrowing.

In contrast, an avalanche debt calculator ignores the balance size and focuses strictly on the Annual Percentage Rate (APR). In this method, you make minimum payments on all accounts but direct every dollar of extra disposable income toward the debt with the highest interest rate. Once that debt is cleared, you take the money you were paying on it and apply it to the debt with the next highest rate. Mathematically, the avalanche method is superior because it aggressively eliminates the most expensive debt first, resulting in the lowest possible total interest paid and the fastest mathematical payoff date.

The limitations of standard web calculators

If you search for an avalanche method debt calculator online, you will find dozens of free tools. While these are helpful for a quick estimate, they suffer from significant limitations for anyone serious about long-term financial planning.

They do not account for the reality of "lumpy" cash flow—variable income, annual bonuses, tax refunds, or unexpected emergency expenses that might reduce your payment capacity for a month. They typically ask you to input a single number for "monthly extra payment" and assume you can pay that exact amount every month for the next three to five years. They do not account for the reality of "lumpy" cash flow—variable income, annual bonuses, tax refunds, or unexpected emergency expenses that might reduce your payment capacity for a month.

Furthermore, web calculators result in data isolation. You input your numbers, get a result, and close the tab. Next month, when you want to check your progress, you have to gather your statements and type everything in again. They function as one-time calculators rather than ongoing financial dashboards, making it difficult to stay consistent with your strategy.

Building a dynamic debt avalanche calculator in Quadratic

Quadratic offers a different approach by combining the familiarity of a spreadsheet with the power of Python and SQL. This allows you to build a calculator that is not only accurate but also connected directly to your financial reality.

The setup

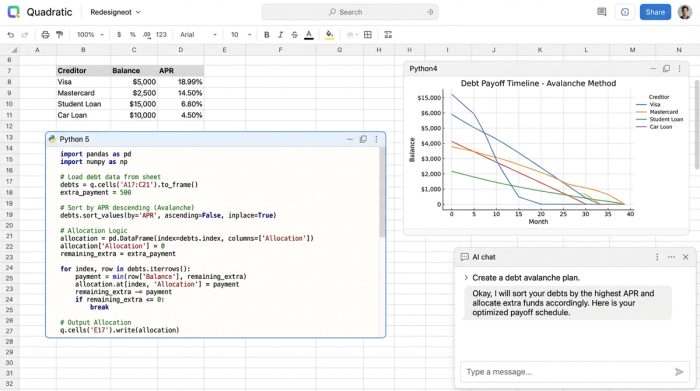

To begin, you set up your grid with the standard columns required for debt tracking: Creditor Name, Current Balance, APR, and Minimum Payment. However, rather than manually updating these figures every month, you can leverage Quadratic’s connectivity.

Step 1: Importing live data

Unlike a standard debt avalanche calculator excel template where you must manually log in to five different banking portals to update your balances, Quadratic allows you to connect to live data sources. You can pull in transaction data or current balances from connected APIs or databases. This ensures that every time you open your dashboard, your "Current Balance" column reflects the actual amount you owe today, not what you owed three weeks ago.

Step 2: The logic (Python/SQL)

This is where the avalanche method comes to life. In traditional spreadsheets, creating a "waterfall" or cascading payment schedule often requires complex, fragile nested formulas. In Quadratic, you can use Python to handle the logic.

You can write a script that automatically sorts your debt dataset by APR in descending order (highest to lowest). Then, the script can iterate through a timeline—month by month—allocating your "Extra Monthly Contribution" to the top row. Once the highest-interest debt reaches zero, the script automatically redirects those funds to the next debt in the list. Finally, you can visualize the data to keep yourself motivated.

Step 3: Visualizing the payoff

Finally, you can visualize the data to keep yourself motivated. You can plot your total debt reduction over time or create a chart comparing "Total Interest Paid" under your current plan versus the avalanche strategy. Seeing the gap between the two lines widens provides a tangible representation of the money you are saving.

Modeling "lumpy" payments and hybrid strategies

One of the distinct advantages of using a programmable environment like Quadratic is the ability to model non-linear scenarios. Life is rarely a straight line, and your debt payoff plan shouldn't be either.

Scenario A: The windfall

Suppose you expect a tax refund in March or a performance bonus in December. A standard web calculator cannot easily factor this in. In your Quadratic model, you can create a "Windfalls" input section. Your Python script can be adjusted to inject these one-time large payments into the specific month they occur. This allows you to see exactly how a single $2,000 payment in March shifts your debt-free date by several months.

Scenario B: The hybrid approach

Sometimes, the strict math of the avalanche method feels too rigid. You might have a small $500 balance that is annoying you, even if it has a lower interest rate. You can program a debt avalanche vs snowball calculator hybrid scenario. This flexibility allows you to optimize for both your finances and your peace of mind.

Key inputs for your calculation

To build a robust model, ensure you have accurate data for the following entities:

- Current Balance: The total principal amount currently owed on the loan or credit card.

- APR (Annual Percentage Rate): The annual rate charged for borrowing. This is the critical sorting factor for the avalanche method.

- Minimum Payment: The contractual minimum you must pay to avoid penalties. Your model must ensure these are covered before allocating extra funds.

- Extra Contribution: The amount of money you have available over and above the minimums to accelerate the payoff.

Conclusion: From calculation to execution

A debt avalanche calculator is only as valuable as its ability to adapt to your changing life. By moving your financial planning into a dynamic tool like Quadratic, you transition from simple calculation to active execution. You gain the ability to import live balances, test different "what-if" scenarios with your income, and visualize the impact of every extra dollar you pay. Instead of wondering when you will be debt-free, you can build a dashboard that shows you exactly how to get there efficiently.

Use Quadratic to build a dynamic debt avalanche calculator

- Automate balance updates: Connect directly to live bank data and APIs to instantly update current balances, eliminating manual data entry each month.

- Apply complex payoff logic with ease: Use Python to automatically sort debts by highest APR and dynamically allocate extra payments, ensuring the most mathematically efficient payoff.

- Model real-world financial scenarios: Easily factor in variable income, bonuses, or unexpected expenses to see their exact impact on your debt-free date.

- Visualize your progress: Create custom charts and graphs to track total debt reduction and interest savings, keeping you motivated and informed.

- Build a flexible, ongoing financial dashboard: Move beyond static calculators to create a dynamic tool that adapts to your evolving financial situation and supports hybrid strategies.

Take control of your debt repayment strategy. Try Quadratic.