When most people search for a car loan interest rate calculator, they are looking for a single number: the monthly payment. It is a quick, transactional query usually performed on a dealer’s website or a generic financial portal. You type in the vehicle price, slide a bar for the down payment, and get a figure—perhaps $550 a month.

However, relying on a static widget creates a "silo gap" in your financial planning. That calculator operates in a vacuum. It does not know your rent, your grocery inflation rate, or your aggressive savings goals. It gives you a number, but it cannot tell you if that number will break your budget three months from now.

To truly assess affordability, you need to move beyond isolated web widgets. By building a dynamic calculator in Quadratic, you can connect financing scenarios directly to your live bank data. This approach shifts the focus from "What is my monthly payment?" to the far more critical question: "Can I actually afford this car given my real-world cash flow?"

The hidden variables: how to calculate interest rate on a car loan

Before integrating your data, it is important to understand the mechanics behind the math. To satisfy the informational intent of how to calculate interest rate on a car loan, you must understand the three specific variables that drive the formula: the principal (the vehicle price minus your down payment and trade-in), the loan term (usually in months), and the annual percentage rate (APR).

Unlike new cars, which often come with subsidized manufacturer incentives (sometimes as low as 0% or 1.9%), used car rates are generally higher and more volatile based on your credit tier and the vehicle’s age.

When you understand these inputs, you can stop guessing and start modeling. Instead of accepting the dealer's printed sheet, you can input these variables into your own environment to see how a 1% variance in APR impacts your bottom line.

Building your calculator in Quadratic: beyond the static widget

Moving from a generic web tool to a Quadratic spreadsheet allows you to retain your data and customize your analysis. This workflow transforms a passive calculation into an active financial model.

Step 1: the setup

Start by setting up your input columns. You will need cells for Vehicle Price, Down Payment, Trade-in Value, Sales Tax, and Interest Rate. Because Quadratic allows you to mix Python and standard formulas, you can create variables that are easy to reference later.

Step 2: the formula

To solve how do you calculate interest rate on a car loan payments, you can use standard financial functions directly in the grid. The PMT function is the industry standard for this. By referencing your input cells, you can instantly generate the monthly payment. If you prefer Python, you can write a short script in a code cell to handle more complex amortization schedules that factor in extra payments.

Step 3: the integration

This is the differentiator. A standard car loan calculator with interest rate inputs stops at the payment amount. In Quadratic, you can connect directly to your bank account or credit card data using built-in integrations. By pulling in your last 12 months of income and expenses, you can derive your actual "free cash flow." You then subtract your calculated car payment from this real-world number. This reveals exactly how the loan fits into your life, not just your theoretical budget.

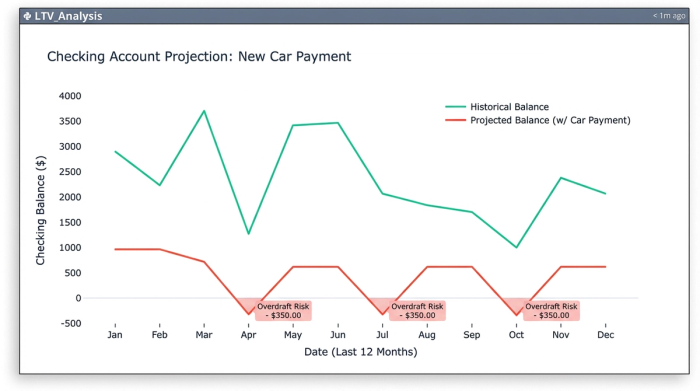

Visualizing the impact: monthly payment vs. free cash flow

The greatest risk in car buying is not the purchase price, but the cash flow pinch. A $600 payment might look affordable on an annual basis, but it could be disastrous during high-spend months like December or August.

Using an interest rate on a car loan calculator inside Quadratic allows you to visualize this risk. You can plot your historical checking account balance on a timeline and overlay the new car payment. This visualization might show that while you are cash-positive on average, the new loan would have pushed you into overdraft fees three times in the last year.

This level of insight is impossible to get from a browser widget. It turns abstract debt into a visual story about your financial health, helping you avoid liquidity crises before signing the paperwork.

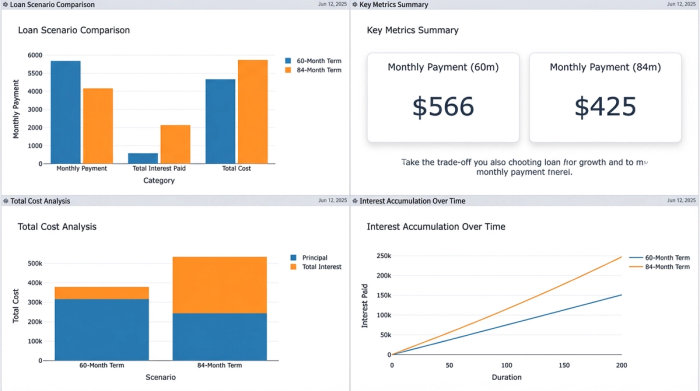

Scenario planning: comparing terms and total interest

Dealers often focus on the monthly payment to distract buyers from the total cost of the car. They may lengthen the loan term to 84 or even 96 months to make a monthly figure appear attractive. You need an interest rate calculator car loan workflow that exposes the long-term reality of these "deals."

In your spreadsheet, you can set up side-by-side scenarios. Column A can represent a 60-month loan at a lower rate, while Column B represents an 84-month loan at a higher rate. By summing the total interest paid over the life of the loan, you will often find that the "cheaper" monthly payment costs thousands more in the long run.

Furthermore, you can model the "upside-down" risk. By estimating a depreciation curve (e.g., the car loses 15% value per year), you can compare the loan balance to the car’s value over time. A robust car loan interest rates calculator in Quadratic will visually demonstrate that a longer term leaves you owing more than the car is worth for several years, trapping you in the vehicle if your life circumstances change.

Validating affordability: the "safe" number

Financial experts often cite rules of thumb, such as the 20/4/10 rule (20% down, 4-year term, payment no more than 10% of gross income). While these are good starting points, they are generic.

With your connected data, you can validate these rules against your specific history. You might find that you spend less on housing than the average person, allowing you to safely allocate 12% to transportation. Conversely, if you have high childcare costs, even 10% might be reckless. Your Quadratic dashboard validates affordability based on your actual transaction history, giving you a "safe" number that is personalized to your unique financial DNA.

Conclusion: don't just calculate—plan

A generic car loan interest rate calculator gives you a number; a connected Quadratic spreadsheet gives you a plan. The difference between financial stress and financial security often lies in the context that standard tools ignore.

By taking the time to build a calculator that respects your income, expenses, and long-term goals, you move from being a passive buyer to an informed analyst of your own life. Stop guessing with static web tools and start building a budget-aware model that ensures your new car is a blessing, not a burden.

Use Quadratic to build a personalized car loan interest rate calculator

- Connect live financial data: Integrate your bank account and credit card data to calculate true affordability based on your actual cash flow, not theoretical numbers.

- Visualize real-world impact: See how a new car payment affects your historical bank balances and projected cash flow, helping you avoid overdrafts and financial strain.

- Compare loan scenarios: Model different interest rates and loan terms side-by-side to understand total costs and identify the best financial fit for you.

- Personalize your analysis: Use a mix of formulas and Python to build a custom car loan calculator that validates affordability against your unique financial history.

- Avoid hidden costs: Clearly see the long-term implications of various loan structures, like total interest paid and the risk of being upside-down on the vehicle.

Stop guessing with static online tools. Build a budget-aware car loan model that fits your life and helps you plan. Try Quadratic.