Most people do not have a single debt; they have a debt portfolio, contributing to the overall household debt outstanding. You might have a student loan servicers’ tab open, a credit card statement in another window, and an auto loan portal on your phone. Trying to mentally aggregate these scattered figures into a cohesive strategy is exhausting and often leads to decision paralysis. This is where a standard online calculator fails and where building a custom loan repayment planner becomes essential.

While online tools are excellent for checking a mortgage rate or a single car payment, they function as "black boxes." They rarely allow you to view all your liabilities side-by-side or account for the reality that your monthly budget fluctuates. By moving your financial data into Quadratic, you can build a Unified Debt Dashboard. This approach combines every liability into a single view, links directly to your real-time budget, and allows you to dynamically model how extra payments impact your debt-free date.

Why standard calculators aren't enough

The primary limitation of most web-based financial tools is the "single loan" limit. If you are trying to pay off three different credit cards and a student loan, you have to use four different calculators. This fragmentation makes it nearly impossible to strategize effectively. You cannot easily see how paying an extra $100 toward one debt affects the aggregate timeline of the others.

Furthermore, there is a significant disconnect between debt calculators and your actual budget. A tool might tell you that paying an extra $500 a month will save you thousands in interest, but it does not help you identify where that $500 is coming from. To truly understand these savings, a robust loan interest calculator is essential. A true loan repayment planner needs to connect to your income and expenses.

This is why a flexible data canvas like Quadratic is superior to a static web form. In Quadratic, you can place your budget data right next to your loan amortization schedules. You are not toggling between browser tabs; you are viewing your entire financial ecosystem in one cohesive grid.

The strategy debate: Snowball vs. Avalanche

When building your planner, it is helpful to understand the two most common repayment methodologies, as your custom tool will allow you to switch between them or create a hybrid approach.

The Debt Snowball method focuses on psychology. The strategy involves listing debts from smallest balance to largest balance. You pay minimums on everything but the smallest debt, which you attack with every available dollar. When that debt is cleared, you roll those payments into the next smallest balance. This creates quick "wins" that keep you motivated. A dedicated debt snowball tracker can help you visualize and maintain this momentum.

The Debt Avalanche method focuses on mathematics. Here, you list debts from highest interest rate to lowest. You attack the debt with the highest rate first (usually credit cards), regardless of the balance size. Mathematically, this saves you the most money over time.

In the real world, you shouldn't be forced to choose a rigid path. Life happens. You might want to clear a small debt for peace of mind (Snowball) and then tackle a high-interest loan (Avalanche). A custom spreadsheet allows you to switch strategies or split surplus cash between debts based on your changing needs, something a standard calculator simply cannot do.

Building your unified dashboard in Quadratic

Creating a custom planner in Quadratic gives you control over the logic and the layout. The goal is to aggregate your data so you can see the total picture.

Step 1: Aggregate the data

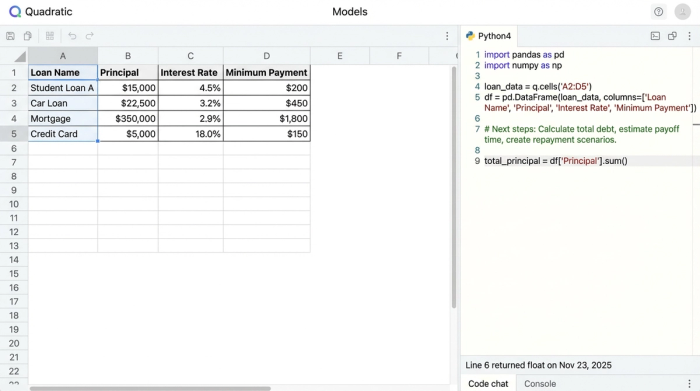

Start by setting up a simple table with columns for Loan Name, Principal Balance, Interest Rate, and Minimum Payment. For example, your table might list a Student Loan at $15,000 (5%), an Auto Loan at $8,000 (4%), and a Credit Card at $2,000 (19%). Seeing these numbers in a single grid is often the first step toward taking control.

Step 2: Calculate the baseline

Using standard spreadsheet formulas or Python directly within Quadratic, you can calculate the payoff timeline for each loan assuming only minimum payments are made. This establishes your "baseline"—the default path if you change nothing about your current habits.

Step 3: The "surplus cash" variable

This is the strategic differentiator. Create a dedicated cell labeled "Monthly Budget Surplus." This cell represents the money left over after your living expenses and minimum debt payments are met. This variable will drive the rest of your model. Unlike a static calculator where you have to re-type numbers to test scenarios, changing this single cell in Quadratic will instantly update your entire repayment timeline.

Modeling your accelerated payoff plan

Once your data is structured, you can begin modeling the future. The power of this loan repayment planner lies in connecting your "Surplus Cash" cell to your loan principals.

You can set up logic to route that surplus cash based on your chosen strategy. In an Avalanche scenario, you would direct the model to apply the surplus to the Credit Card first because it has the 19% interest rate. In a Snowball scenario, you would route that same cash to the Credit Card simply because it has the lowest balance ($2,000).

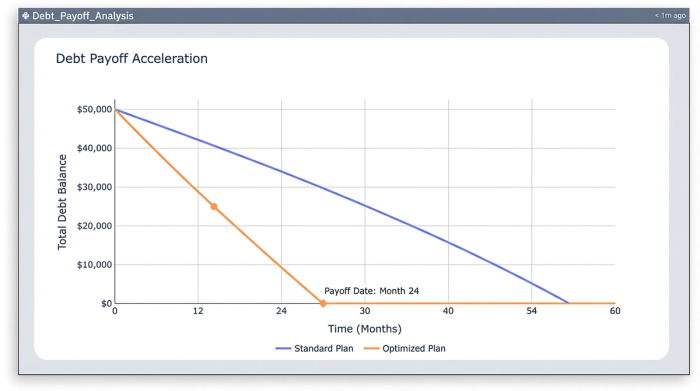

Because Quadratic supports advanced visualization, you can graph these outcomes. You can create a "burn down" chart that displays two lines: one representing your Standard Plan (minimum payments) and a steeper line representing your Optimized Plan (minimums + surplus). This visual proof is incredibly powerful. It transforms abstract numbers into a clear image of time saved, showing you exactly how much faster the Optimized line hits zero compared to the Standard line.

Analyzing the "cost of debt" savings

While monthly payments are important, the true cost of debt is the total interest paid over the life of the loans. A comprehensive loan repayment planner should highlight this metric.

In your Quadratic sheet, you can sum the total interest for all loans under both the baseline and the optimized scenarios. This leads to the "aha" moment for many users. You can experiment by increasing your "Monthly Budget Surplus" cell by just $50. Immediately, the model recalculates, and you might see that this small monthly sacrifice saves you $1,500 in total interest over three years.

By visualizing the "Cost of Debt," you shift your mindset from "making payments" to "buying freedom." It turns debt repayment into an optimization game where you can clearly see the return on investment for every extra dollar you pay.

Conclusion

Financial freedom is rarely achieved by accident; it requires a plan you can see, understand, and control. Moving from static web calculators to a dynamic, multi-loan workspace allows you to stop guessing and start strategizing.

By building a Unified Debt Dashboard in Quadratic, you gain the ability to model different scenarios, adapt to budget changes, and visually confirm that you are on the fastest path to zero balance. Don't just pay your bills—optimize them. Start building your custom planner in Quadratic today and take ownership of your financial future.

Use Quadratic to Build Your Custom Loan Repayment Planner

- Aggregate all your debts in one place. Create a unified dashboard to view every loan, interest rate, and minimum payment side-by-side, eliminating fragmentation.

- Connect debt strategy to your real-time budget. Integrate your income and expenses directly into your planner to identify surplus cash for accelerated payments.

- Dynamically model payoff scenarios. Instantly see how extra payments impact your debt-free date and total interest saved, without re-entering numbers.

- Customize repayment strategies. Flexibly switch between debt snowball, avalanche, or hybrid methods to adapt to your financial goals and changing needs.

- Visualize your progress. Generate "burn down" charts to clearly compare your standard payment plan against optimized, faster payoff timelines.

- Analyze the true cost of debt savings. Quantify the total interest saved by making extra payments, turning debt repayment into a clear optimization game.

Ready to take control of your debt? Try Quadratic.