Buying a home is likely the largest financial commitment you will ever make, yet the tools available to analyze this decision are often surprisingly opaque. Most homebuyers rely on free online widgets found on real estate listing sites. These "black box" calculators hide the underlying math, rely on rigid assumptions, and isolate the mortgage data from the rest of your financial life. They tell you what a payment might be, but they rarely help you understand if you can actually afford it.

The problem with standard tools is fragmentation. You might use one website to estimate monthly payments, another to view an amortization schedule, and a third to guess at tax implications. Worse, these tools usually rely on estimated inputs rather than your real financial data. The solution is to take control of the math by building a custom mortgage with interest calculator in Quadratic, which provides the best financial calculators for mortgage planning. This approach allows you to model principal, interest, taxes, and extra payments in a single, transparent view while syncing with your actual cash flow to test true affordability.

Breaking down the components of a mortgage payment

Before building the calculator, it is essential to understand the variables that dictate your monthly cash outflow. A robust mortgage calculator with principal and interest must account for more than just the loan repayment. It needs to factor in the "PITI" stack: Principal, Interest, Taxes, and Insurance.

Online listing sites often provide low estimates for the "T" and "I" portions of this equation to make a property appear more affordable. When you build your own tool, you gain the flexibility to input the exact property tax rate for the specific municipality you are looking at, as well as accurate homeowners insurance quotes. A comprehensive mortgage calculator with interest and taxes ensures you aren't blindsided by the variable costs that exist on top of your bank payment.

Additionally, many loans come with HOA fees or private mortgage insurance (PMI). A standard mortgage payment calculator with interest often buries these details in the fine print. By defining these variables explicitly in your own spreadsheet, you ensure that every dollar is accounted for before you sign a contract.

Building your calculator: the core formula

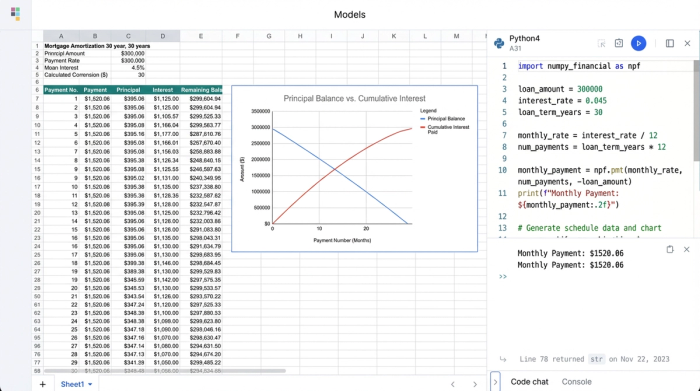

Moving from theory to practice involves setting up your inputs and defining the relationship between them. In Quadratic, you start by creating specific cells for your variables: Loan Amount, Annual Interest Rate, and Loan Term (typically 15 or 30 years).

Once the inputs are set, you can use standard financial formulas to calculate mortgage payment with interest rate variables. The PMT function is the standard method for determining the fixed monthly payment required to pay off a loan over a set term. Unlike a web widget where the output is a static number, building this in a spreadsheet gives you transparency. You can click on the cell and see exactly how the inputs drive the output.

This transparency is vital when comparing offers. A mortgage loan calculator with interest that you build yourself allows you to instantly toggle the interest rate input to see how a 0.5% rate hike impacts your monthly bottom line. By manually configuring a mortgage calculator with interest rates as dynamic variables, you move from passive observation to active scenario planning.

Visualizing the amortization schedule

Knowing your monthly payment is important, but understanding how that payment is split between the bank and your home equity is where the real insight lies. To visualize this, you expand your single monthly payment calculation into a full amortization schedule calculator—a "waterfall" of rows representing every month of the loan term.

In the early years of a standard 30-year mortgage, the vast majority of your payment goes toward interest. By calculating the interest portion (Loan Balance multiplied by the Monthly Interest Rate) for each row, you can see exactly how slowly your principal decreases.

This structure also allows for flexibility in loan types. For example, real estate investors often use interest-only loans to maximize cash flow. You can easily modify your row logic to simulate an interest only loan calculator, where the principal balance remains flat for a set period. Comparing a standard amortizing loan against a mortgage calculator with interest only scenario side-by-side helps you understand the long-term cost of lower short-term payments.

Modeling scenarios: extra payments and payoff dates

One of the distinct advantages of using Quadratic over a fragmented web tool is the ability to conduct "what if" analyses without losing your previous work, such as with a pay off mortgage faster calculator.

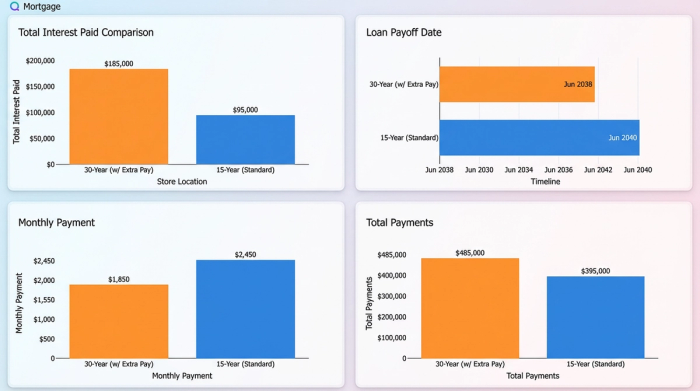

In your custom calculator, you can add an "Extra Principal" column to your amortization schedule. You can then model different scenarios, such as adding $100 a month or applying a single annual lump sum from a work bonus. Because the sheet is dynamic, you will instantly see the "Payoff Date" row move up and the "Total Interest Paid" figure drop.

This allows for powerful comparisons. You can duplicate your sheet to compare a 30-year loan with aggressive extra payments against a standard 15-year loan. This level of granularity helps you decide whether to commit to a higher mandatory payment or maintain the flexibility of a longer term with voluntary extra contributions.

Determining affordability with real data

The most significant limitation of a standard online calculator is that it does not know your spending habits. It operates in a vacuum, assuming that if your debt-to-income ratio is below a certain threshold, the loan is affordable. Quadratic changes this by allowing you to work with real data.

Because Quadratic integrates with external data sources, you can pull in your actual bank transaction history or export a CSV of your last year’s spending. Instead of guessing at your discretionary income, you can overlay your projected mortgage payment on top of your historical cash flow.

This acts as a reality check. You might technically qualify for a loan, but visualizing that payment against your actual grocery, travel, and utility spending might reveal a different story. This transforms the exercise from a theoretical calculation into a true affordability test based on your unique lifestyle.

Tax implications and final analysis

Finally, a comprehensive analysis includes the potential tax benefits of homeownership. While tax laws are complex and subject to change, your amortization schedule provides the raw data needed to estimate deductions. By summing the "Interest" column for the first 12 rows, you can project your total interest expense for the first year.

This effectively turns your sheet into a preliminary tax calculator with mortgage interest deduction estimation. For many buyers, the ability to deduct mortgage interest can slightly offset the cost of the monthly payment. Seeing the raw dollar amount of interest you will pay—and potentially deduct—adds another layer of data to the "rent vs. buy" decision.

Conclusion

A mortgage is a massive financial product that deserves more scrutiny than a generic internet widget can provide. By moving your analysis into Quadratic, you stop relying on black boxes and start making decisions based on transparent math and your own financial reality. Whether you are comparing interest rates, planning extra payments, or testing affordability against real spending data, building your own tool gives you the confidence to move forward. To start modeling your loan scenarios immediately, you can use the Quadratic mortgage calculator template or other personal finance templates to customize your analysis today.

Use Quadratic to model your mortgage with interest

- Build a transparent mortgage calculator: Move beyond opaque online tools by creating a custom calculator that clearly displays all underlying math, ensuring you understand every component of your payment.

- Account for all costs: Accurately model principal, interest, taxes, insurance, HOA fees, and PMI in one place, avoiding hidden costs found in generic estimates.

- Perform dynamic "what if" scenarios: Instantly compare different interest rates, loan terms, and the impact of extra payments on your monthly cash flow and total loan cost.

- Assess true affordability: Integrate your actual bank transaction history and spending data to overlay projected mortgage payments, providing a realistic view of how a loan fits your financial life.

- Visualize amortization and tax benefits: Generate full amortization schedules to see how principal and interest are paid over time, and easily estimate potential mortgage interest tax deductions.

Take control of your home financing decisions. Try Quadratic to start building your custom mortgage analysis.