Table of contents

- Runway vs. emergency fund: why the difference matters

- The inputs: preparing your data in Quadratic

- How to perform a dynamic runway calculation

- Advanced scenario modeling: "what if?"

- Interpreting your runway: the phases of freedom

- Conclusion: become the CEO of your own life

- Use Quadratic to calculate your personal cash runway

In the startup world, "runway" is the most critical metric a founder watches. It is the countdown, usually measured in months, until the bank account hits zero. It dictates whether a company is in survival mode or growth mode. Interestingly, this concept is often missing from personal finance. Most advice centers on the "Emergency Fund"—a defensive, static number meant to protect you from a broken boiler or a medical bill.

However, if you view your life through the lens of a business, an emergency fund is insufficient for strategic planning. To make significant life pivots—such as quitting a toxic job, launching a freelance career, or taking a sabbatical—you need to move from defense to offense. You need a runway calculation.

This is not just about ensuring you can pay the rent next month. It is about modeling financial freedom. By treating your household finances like a startup, you can use data to determine exactly how long you can survive and thrive without a primary income source. This article explores how to use Quadratic to build a dynamic, automated workflow that turns your financial data analytics into a roadmap for independence.

Runway vs. emergency fund: why the difference matters

Before diving into the numbers, it is essential to distinguish between a standard safety net and a true runway. An emergency fund is typically a fixed amount of cash, such as $10,000, set aside for unexpected disasters. It is a static number that sits in a savings account, waiting for something to go wrong.

A personal runway is a timeline. It is a dynamic metric derived from a specific formula: Liquid Assets / Monthly Burn Rate.

Calculating runway answers a different set of questions. Instead of asking, "Can I afford this car repair?" it asks, "Do I have the capital to negotiate for a higher salary?" or "Do I have the time to build a product before I need to find a job?"

When you calculate cash runway, you are quantifying your leverage. If you have three months of runway, you are likely forced to take the first job offer that comes along. If you have eighteen months, you have the strategic freedom to wait for the right opportunity or build something of your own. To effectively calculate runway, you must adopt the mindset of a CFO, treating your personal savings as "capital" and your living expenses as "burn rate."

The inputs: preparing your data in Quadratic

To get an accurate number, you need to aggregate your data. A back-of-the-napkin math equation is rarely accurate because it misses the nuances of spending habits and hidden assets. Using a modern tool like Quadratic allows you to connect to real data sources or import CSVs from your bank, ensuring your model is based on reality rather than guesswork.

Step 1: Determine liquid assets

Your first task is to calculate your total accessible capital. This includes checking accounts, savings accounts, and money market funds, which are examples of liquid assets. In this context, you should generally exclude assets that are locked up or penalized for early withdrawal, such as 401(k)s or real estate equity. You are looking for liquidity—money you can spend tomorrow to keep the lights on.

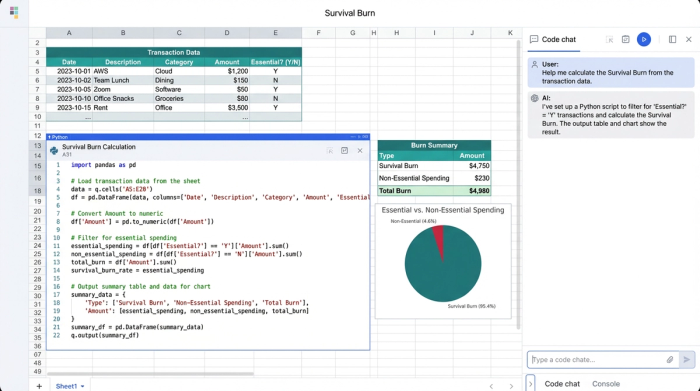

Step 2: Calculate your burn rate

This is where most people make mistakes. Your "Gross Burn" is what you spend right now to maintain your current lifestyle, including dining out, entertainment, and travel. However, your "Survival Burn" is the number that matters for a crisis or a lean startup phase.

In Quadratic, you can ingest your transaction data and use Python or SQL queries to filter expenses automatically. For example, you can use a weekly spending tracker to query your last six months of spending, filter out categories like "vacation" or "luxury," and arrive at a precise average of your essential monthly expenses. This distinction is vital when you learn how to calculate runway because it gives you two different timelines: how long you can live comfortably versus how long you can survive if you cut all non-essential costs.

How to perform a dynamic runway calculation

The basic mathematics of a runway are simple division. If you have $50,000 in liquid cash and your survival burn rate is $5,000 per month, you have 10 months of runway. However, life is rarely linear. Expenses fluctuate, unexpected costs arise, and you might have partial income streams.

This is why you need an app that calculates cash runway automatically using dynamic financial modeling with variables rather than static cells. In Quadratic, you can build a workflow that adapts to changing inputs.

1. Ingest data: Pull in your current liquid cash balance and your recent average monthly essential expenses.

2. Set variables: Instead of hard-coding numbers, create input cells for variables like "Projected Monthly Spend" or "Side Hustle Income."

3. Run the model: Use formulas to divide your total cash by your net burn rate. Because Quadratic supports Python, you can write a script that updates your runway instantly as you adjust the variables.

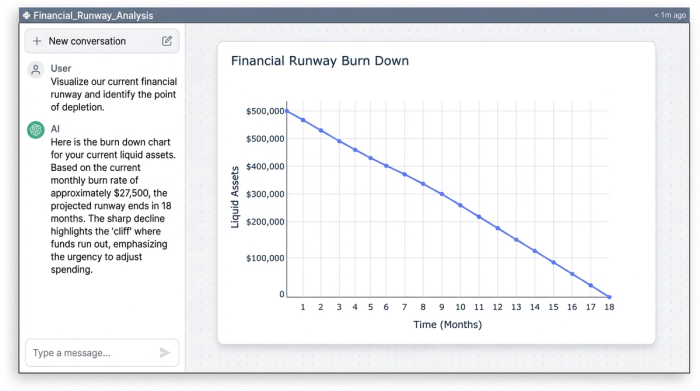

Beyond the number, visualization is key. A single number like "14 months" can feel abstract. By plotting your data on a line graph, you can visualize the "burn down" of your cash over time. Seeing the slope of the line helps you visualize the "cliff"—the exact date your money runs out. This visual feedback loop is often what motivates people to lower their burn rate to flatten the curve and extend their timeline.

Advanced scenario modeling: "what if?"

Static Excel templates often fail when you need to answer complex "what if" questions. You usually have to duplicate tabs or break formulas to test different theories. Because Quadratic combines the grid interface with code, you can run sophisticated financial forecasts & scenarios to see how different decisions impact your future.

Scenario A: The lean startup mode

What happens to your runway if you cut your budget by 20%? You can adjust your "Burn Rate" variable to reflect a lean budget—removing recurring charges like subscriptions, dining out, and gym memberships. The model will instantly recalculate, perhaps showing that you gain an extra four months of freedom simply by tightening your belt.

Scenario B: The "soft landing"

Runway isn't always about having zero income. What if you quit your job but picked up a small freelance contract? You can add a "Partial Income" variable to your model. Even a modest income of $2,000 a month can drastically reduce your net burn rate, potentially doubling your runway.

Scenario C: Debt and large expenses

Should you pay off your car loan before you quit your job? This is a classic optimization problem. Paying off the debt reduces your liquid assets (shortening runway) but also reduces your monthly burn (extending runway). Using a debt snowball tracker allows you to model this trade-off instantly to see which option mathematically yields the longest survival time.

Interpreting your runway: the phases of freedom

Once you calculate cash runway, you need to understand what the number implies for your life strategy.

0–3 Months (Survival): You are dependent on your next paycheck. You have very little leverage and cannot afford to take risks. Your immediate goal should be to lower burn or increase liquidity.

3–12 Months (Flexibility): You have entered a phase of flexibility. You have enough cash to leave a toxic work environment, but you need a plan to replace that income relatively quickly. You have breathing room, but the clock is ticking loud enough to hear.

12–24+ Months (Strategic Freedom): This is the sweet spot for aspiring entrepreneurs. You have enough runway to build a business, pivot careers, or take a mini-retirement without the pressure of immediate revenue.

Conclusion: become the CEO of your own life

Emotions often cloud financial decisions. We stay in bad jobs because we fear the unknown, or we delay starting a business because we feel we "don't have enough money yet." A runway calculation cuts through the fear with cold, hard data. It gives you the confidence to make emotional life decisions with logical backing.

Don't rely on mental math or static spreadsheets that break the moment your situation changes. By using Quadratic, you can build a dynamic, visual financial forecast template of your financial future that updates as your life evolves. When you know your numbers, you stop just surviving and start operating like the CEO of your own life.

Use Quadratic to calculate your personal cash runway

- Connect directly to your financial data or import CSVs for real-time, accurate liquid asset and expense tracking.

- Automate burn rate calculation by using Python or SQL to filter and categorize transaction data, distinguishing essential "survival burn" from discretionary spending.

- Model complex "what if" scenarios instantly to understand how changes in income, expenses, or debt payments impact your runway without breaking formulas.

- Visualize your financial timeline with dynamic charts that show your cash burn down, helping you plan for strategic life pivots with confidence.

- Build a dynamic forecast that updates automatically with changing inputs, providing a continuously accurate roadmap for your financial independence.

Ready to take control of your financial future? Try Quadratic.